What Drives Utility Solar Growth in a Post-ITC-Extension World?

March 24, 2016 | posted by The Institute

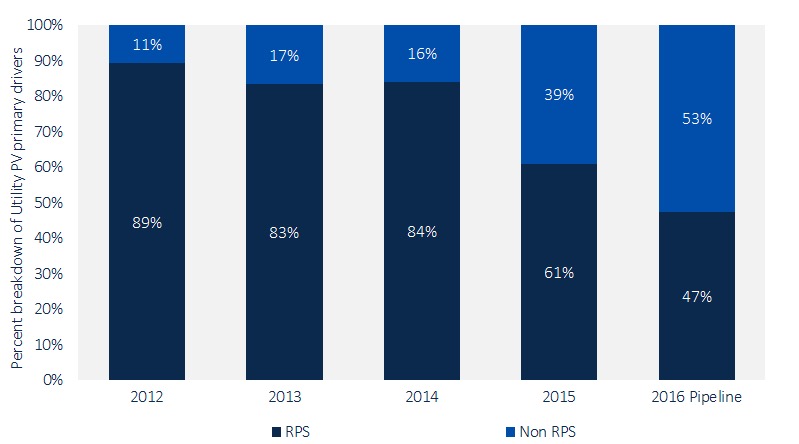

Through 2015, 77 percent of the 13.9 gigawatts of utility solar operating in the U.S. has been driven by state renewable portfolio standards. But according to GTM Research’s latest report, The Next Wave of U.S. Utility Solar, 52 percent of utility PV installations in 2016 will be driven by three distinct drivers outside of states’ RPSs

.

And those non-RPS drivers are all emerging because utility-scale solar has become dirt-cheap for utilities (and large corporate customers too).

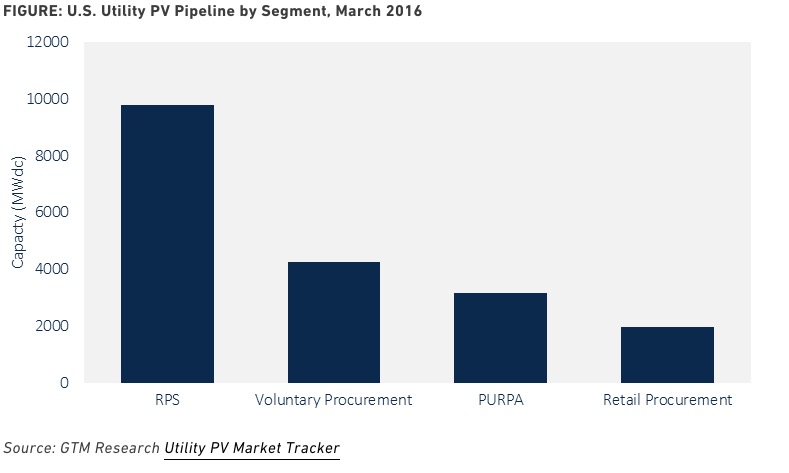

According to GTM Research's Utility PV Market Tracker, 2016 power-purchase agreements are being signed at values between $35 and $60 per megawatt-hour in a diversified demand landscape where more than 50 percent of the project pipeline comes from the following non-RPS drivers: voluntary utility procurement outside of RPS obligations; qualified facility development enabled through the federal Public Utility Regulatory Policies Act; and retail customer procurement.

Voluntary procurement

Voluntary procurement is quickly emerging as the largest driver of non-RPS solar, as investor-owned utilities and municipal and cooperative utilities procure solar to replace aging coal fleets, and as munis and co-ops seek to hedge against natural-gas price volatility.

And those non-RPS drivers are all emerging because utility-scale solar has become dirt-cheap for utilities (and large corporate customers too).

According to GTM Research's Utility PV Market Tracker, 2016 power-purchase agreements are being signed at values between $35 and $60 per megawatt-hour in a diversified demand landscape where more than 50 percent of the project pipeline comes from the following non-RPS drivers: voluntary utility procurement outside of RPS obligations; qualified facility development enabled through the federal Public Utility Regulatory Policies Act; and retail customer procurement.

Voluntary procurement

Voluntary procurement is quickly emerging as the largest driver of non-RPS solar, as investor-owned utilities and municipal and cooperative utilities procure solar to replace aging coal fleets, and as munis and co-ops seek to hedge against natural-gas price volatility.

PURPA implementation is different for each utility and state market. Since there is regional variation in wholesale power pricing and each utility uses its own distinct PPA price methodology, only a few PURPA markets are attractive to developers at the current juncture.

On the other hand, in states with favorable conditions, utilities are unable to cap the influx of projects that apply to come on-line through PURPA. On more than one occasion, utilities have pushed back against the flood of qualified PURPA projects that enter the interconnection queue and petitioned the state utility commission to reduce the length of standard contracts and decrease the maximum system size for qualified PURPA projects in order to make it more difficult for new project development to occur.

PURPA will drive new utility solar as more developers are able to achieve adequate returns from standard contracts. As new PURPA markets emerge, there will be a growing risk of pushback by utilities seeking to slow project development and control the amount of renewable power they procure.

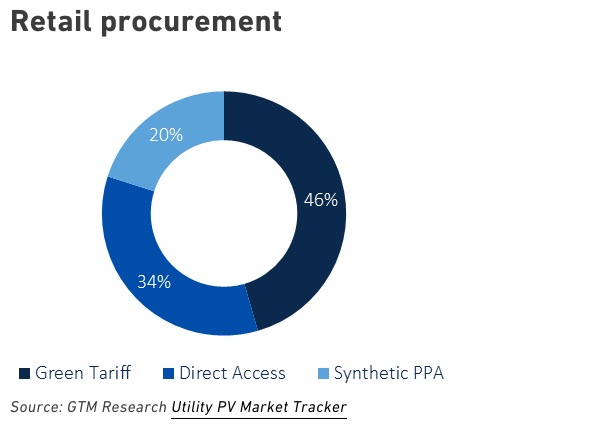

Retail procurement has the biggest growth potential for utility solar. Ninety-eight megawatts of retail procurement projects came on-line in 2015, but there are 2 gigawatts' worth of projects (11 percent of the current utility PV pipeline) currently in development with a corporate entity, school or city. Retail procurement projects are being developed through three different kinds of mechanisms.

First, 46 percent of retail procurement projects are being developed by utilities, like NV Energy and Duke Energy, through green tariff arrangements to resell power from a utility-scale solar project to a single company. These green tariff programs allow the utilities to retain these valuable corporate customers rather than lose them to independent power producers (IPPs).

Second, most notably in California, the Utility PV Market Tracker shows 46 percent of projects are via direct access. To date, the University of California, Apple and Kaiser Permanente have all taken advantage of direct-access rules to procure offsite solar from utility-scale developers such as First Solar and NextEra Energy.

Finally, 20 percent of retail procurement projects are leveraging synthetic PPAs. Many developers are opting to sell power to the wholesale electricity market and also sign a third-party agreement with a corporate entity and provide a floor and/or ceiling for the electricity price.

Over the next several years, we expect to see retail procurement make up a growing percentage of U.S. utility solar as corporations negotiate such deals with independent IPPs to control and lower their energy costs.

Over the course of 2016, as utility-scale solar PPAs become increasingly cost-competitive and corporations’ comfort with new procurement mechanisms increases, non-RPS procurement mechanisms are expected to account for a growing share of the utility-scale solar outlook. With 52 percent of the current utility solar pipeline coming from these three drivers, GTM Research expects the developer landscape to diversify as smaller companies, able to leverage one or more of these market drivers in specific states, build out large pipelines of voluntary procurement, PURPA and retail procurement projects.